This module demonstrates the gap analysis technique and its use in measuring and reporting interest rate risk (IRR) for a financial institution (FI). IRR exists when changes in interest rates impact on the FI's net interest income (NII) for the reporting period. The impact of interest rate changes on the capital value of assets and liabilities is covered under the duration method.

An example balance sheet is shown in figure 1a, Excel Web App #1. The financial data worksheet includes a categorised balance sheet in the range B2:D19 (red border), and associated NII for balance sheet items in column F . Interest rate details and repricing periods are also included.

Interest rate sensitivity depends on the time to repricing (change of interest rate) for each asset and liability item. For example, Government bonds (line 4) have a fixed coupon, and interest income is fixed until maturity in five years. A change in market rates in the next 12 months will not change the bond coupon income. On the other hand, the fixed rate loans item matures in 5 months, and new loans issued would then be set to the prevailing fixed rate at that time.

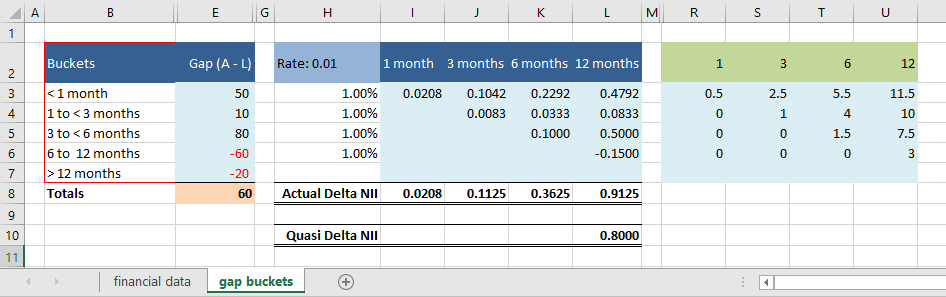

To group items into chronological order of repricing, a time interval, say the next 12 months can be split into intervals, and items repricing in each interval can then be grouped. These time based groups are often called "gap buckets".

Copyright © 2011 – 2024 ♦ Ian O'Connor, Central Gippsland | Privacy policy